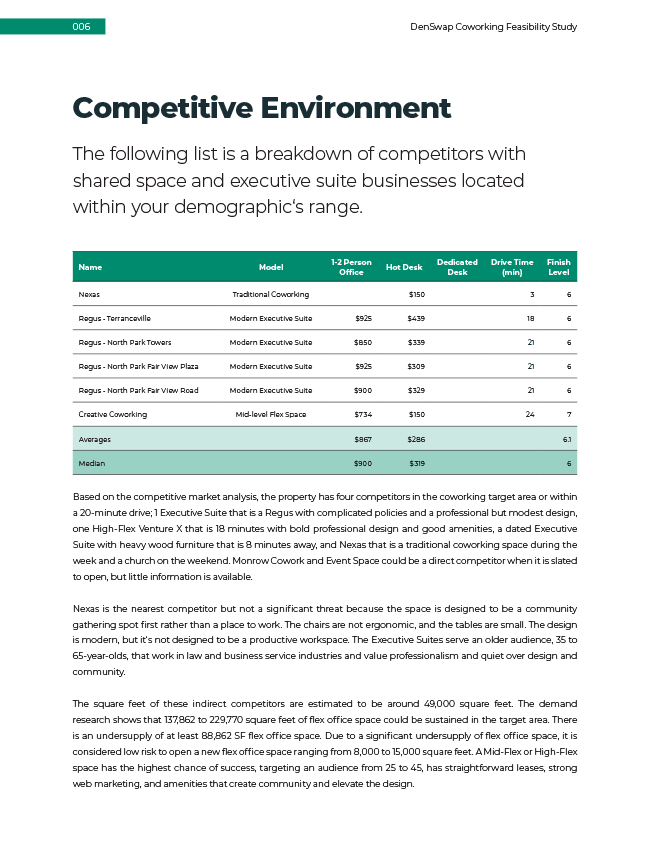

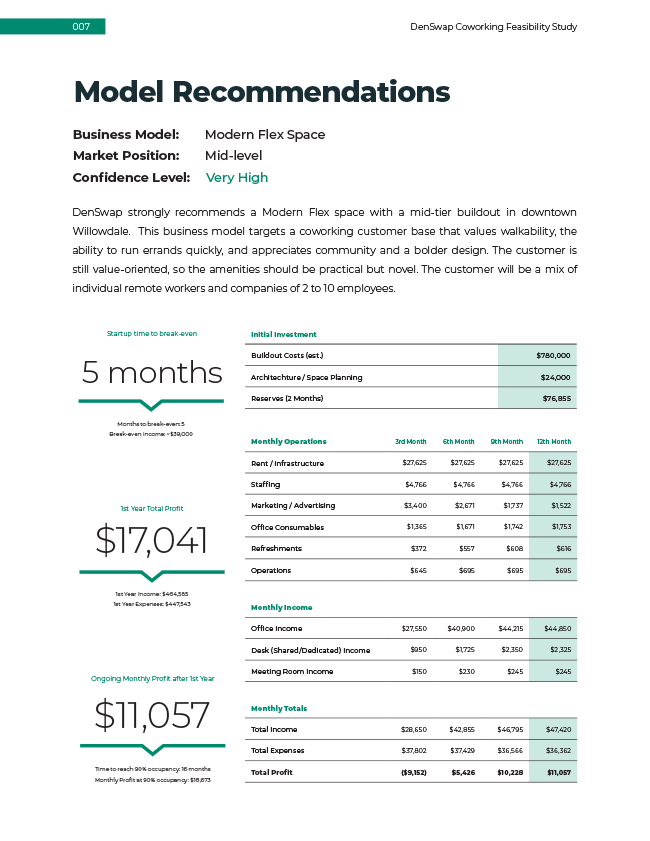

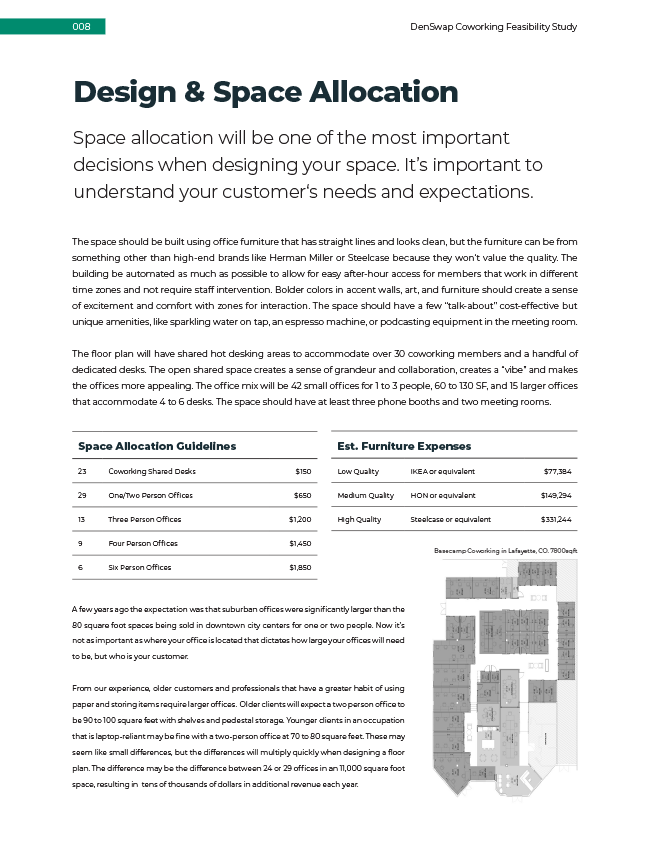

How to fund your next coworking space

As an established coworking owner, you’re in a much better position to get funding for expanded campuses than those starting from scratch. Your record of success will be instrumental in getting loans (collateralized or not), and you have a few more options available to you that new entrepreneurs don’t. Here are some of the options available to you as an existing owner.

Get a bespoke funding plan for your next space from our Buyer Services team.

Reach out and get started on fundingTraditional SBA Loans

Small Business Administration (SBA) loans offer a practical method of small business financing for business owners looking to expand their business. You can use the funds to not only fund the purchase of the business but to cover buildout costs or to use as working capital once you launch.

SBA small business loans offer attractive repayments terms and low interest rates. The loans are typically not directly from the SBA. Rather, the SBA encourages banks to lend to small business owners with preferable terms and multiple loan options. In return, the SBA guarantees 75 to 85 percent of the loan for the bank if the loan defaults.

As an existing owner, you have two options for SBA loans – Working Capital and 7(A).

Working Capital loans offer $75,000 – $150,000 for business operations. These loans provide the same government guarantee and low interest rates as traditional SBA loans, but they can close in as little as 45 days — about half the time it takes to close a traditional SBA loan. Unlike other business loans that a require 20-30 percent down payment and must be secured by personal collateral, Working Capital loans only need 10 percent down and are secured by your business assets.

7(A) loans are more common and have a cap of $5 million, so you’re able to purchase larger and more profitable spaces. They come with low-interest rates, a down payment requirement, longer repayment terms, a collateral component and have a cap of $5 million. This loan program can be combined with other funding options such as rollover for business start-ups.

Keep in mind – these loans are backed by the government so expected increased paperwork and endless amounts of hoops to jump through. If you have all your paperwork in order and are a perfect candidate you might be able to get a 7(A) loan completed in a month, but expect it to take up to 3-4 months. Working capital loans take about half the time a 7(A) loan does.

Seller Financing

Seller financing involves the seller loaning the buyer a certain percentage of the sale as a loan by not receiving it as an upfront cash payment. The buyer makes a down payment for the business to take control and then the remaining amount is paid out to the seller in monthly or quarterly payments with interest, generally 5-7%.

For example, a business sells for $5 million. The buyer makes a down payment of 3 million and the remaining 2 million is paid in monthly installments over the next 5 years carrying a 5% interest rate.

As you might expect, seller financing is a much more personal and intimate experience than a traditional bank loan. Most of it comes down to trust – does the seller trust you as the owner of a coworking chain to hold up your end of the bargain, stay open long enough to get their money back, and continue the community they’ve started? Even with an ironclad contract, we’ve seen sellers back out of a deal because they weren’t comfortable extending that credit to their buyers. It’s a case-by-case basis.

Short-term Online Business Loans

If other financing options fall through, and your existing chain has a steady cash flow to borrow against, consider looking into a short-term business loan. A new crop of online business lenders are making loan decisions by utilizing algorithms, predictive modeling, data aggregation and electronic payment technology – all to determine how risky it is to loan you money. They still look at traditional factors such as your personal credit history and business metrics, but layer in non-traditional data points to build their models.

While you can expect to have a higher interest rate from these sources of capital, there’s typically no collateral required. Additionally, the transparency in pricing and time saved in accessing capital can help acquire the funds you need to jump on the perfect deal while other potential buyers are still working on traditional funding.

401(k) Financing

Although we don’t often see this option used among existing coworking owners, 401(K) funding is an option for you. 401(k) business financing, also known as Rollovers for Business Start-ups (ROBS), is a small business and franchise funding method. ROBS allows you to draw money from your retirement account in order to start or buy a business without incurring an early withdrawal fee or tax penalty. This is not a loan; ROBS just gives you access to your own money so you can build your business without going into debt.

To access your money without triggering an early withdrawal fee or tax penalty, a ROBS structure must first be put in place. The structure has multiple moving parts, each of which must meet specific requirements to stay compliant with the IRS.

Get the funding you need.

If you’re looking for funds to purchase a coworking space, give us a call. We have contacts for SBA and online funding sources who understand the industry and are willing to work with you. We’ve been here before for our own spaces and know what it’s like to start from scratch – we’ve even funded new spaces with credit cards and family loans when we were young and hungry. Reach out today and let’s help get you started on the next stage of your coworking brand.