An owner watches occupancy drift down quarter after quarter. Refinancing conversations get harder. The traditional playbook still runs: extend the lease term, hold the rent, wait for the cycle to turn. But this time the results keep diminishing. The asset functions fine. The capital stack is manageable. The market just reorganized around different use expectations, and every month spent managing the financial symptoms is a month the repositioning window gets narrower.

That is the most expensive misdiagnosis in commercial real estate right now.

The real risk most CRE owners carry in a structurally shifting market is not leverage or liquidity. It is holding an asset configuration the evolving market has stopped rewarding.

The Misdiagnosis: Treating a Positioning Problem Like a Capital Problem

When performance deteriorates, the institutional reflex kicks in. Restructure the debt. Negotiate concessions. Tighten operating costs. Pursue a loan extension and buy time.

Rational responses to cyclical stress, all of them. The problem is that what looks like cyclical stress increasingly has structural roots. Office valuations ended 2024 down 11% nationally, and the pressure is concentrated in assets where the gap between physical configuration and current demand patterns keeps widening.[1] Extend-and-pretend strategies have become so widespread that the Federal Reserve has studied the phenomenon as a systemic concern.[2]

The financial pressure is real. But it is the symptom.

Owners who pour energy into managing the capital structure of a misaligned asset are treating the fever while the infection spreads. Demand misalignment is the disease. And the longer it goes undiagnosed, the fewer options remain.

Financial stress tells you something is wrong. Only demand analysis tells you what is actually wrong.

The Real Risk Framework: Financial Exposure vs. Alignment Exposure

Every commercial asset carries two distinct risk profiles. Most owners track one of them obsessively and never formally test the other.

Financial exposure is the first: debt service coverage, loan maturity timing, cap rate compression, interest rate sensitivity. This is the territory owners and their lenders live in. The spreadsheets are detailed. The models are sophisticated.

Alignment exposure is harder to quantify and easier to ignore. Does the physical configuration of this asset match what the local market actually demands? Are the tenants this building was designed to attract still looking for space? Has the competitive set shifted in ways that make this asset's value proposition obsolete? These questions don't fit cleanly into a model, so most owners skip them.

During stable markets, alignment exposure stays quiet. Lease renewals happen. Absorption stays positive. Nobody questions whether the asset fits.

Once the market starts shifting structurally, alignment exposure compounds faster than financial exposure and resolves more slowly. Meketa Investment Group's analysis of the office sector describes this dynamic plainly: the structural shifts in how tenants use space have created a bifurcation where some assets face permanent demand impairment regardless of capital market conditions.[3] Regional banks are now triaging office portfolios based not just on financial metrics but on whether the underlying assets can attract tenants at all.[4]

That distinction is the one that matters. Financial exposure responds to financial tools. Alignment exposure does not. Refinancing cannot fix a building the market has moved past.

And the compounding works against you. Each quarter of misalignment erodes not just income but optionality. The pool of viable repositioning strategies shrinks. The capital required to execute grows. The competitive set adjusts while you hold still.

What Smart Operators Do Differently

Owners who navigate structural shifts successfully share one trait: they reframe the risk question before committing to a course of action.

Predicting where the market is going is genuinely hard. Testing whether your asset matches what the local market wants right now is not. One is a forecast. The other is a measurement. Smart operators replace the prediction problem with a validation problem - and they do it before capital is committed, not after.

So the question shifts from "what is the market going to do?" to "what is this asset positioned to deliver, and does the local market actually want that?" The second question has an answer you can get before spending a dollar. PIMCO's 2025 outlook noted that the bifurcation between assets aligned with current demand and those that are not has become the defining variable in CRE performance, more predictive than location or vintage alone.[5]

For many owners, the validation exercise surfaces a specific finding: local demand has shifted toward flexible workspace configurations that their current asset does not offer. Coworking and flex space have absorbed a meaningful share of what used to be conventional office demand. Tenants who would have signed a five-year lease in 2019 now want shorter commitments, shared amenities, and operational flexibility.

That finding changes the decision tree entirely. The owner is no longer choosing between "hold and hope" and "sell at a loss." A third path appears: reposition toward the demand that actually exists.

But that path only appears if you test for it.

The owners who lose the most in a structural shift are not the ones who chose wrong. They are the ones who never tested.

Test Alignment Before You Commit Capital

Before spending on design, construction, or a repositioning commitment you cannot easily reverse, test whether your asset is positioned for what the market actually wants.

Your lender can model the financial scenarios. What they cannot tell you is whether converting 20,000 square feet to coworking or flex space will find tenants, what pricing the local market supports, or whether your specific building's configuration and location align with where flexible workspace demand is actually concentrating. Financial risk analysis and positional risk analysis are separate exercises, and confusing them is exactly how owners end up solving the wrong problem.

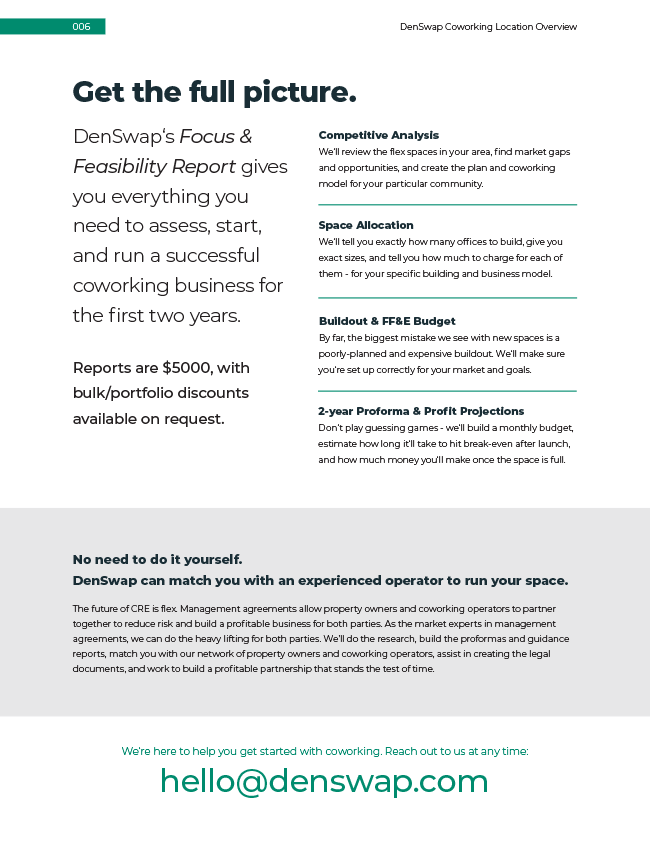

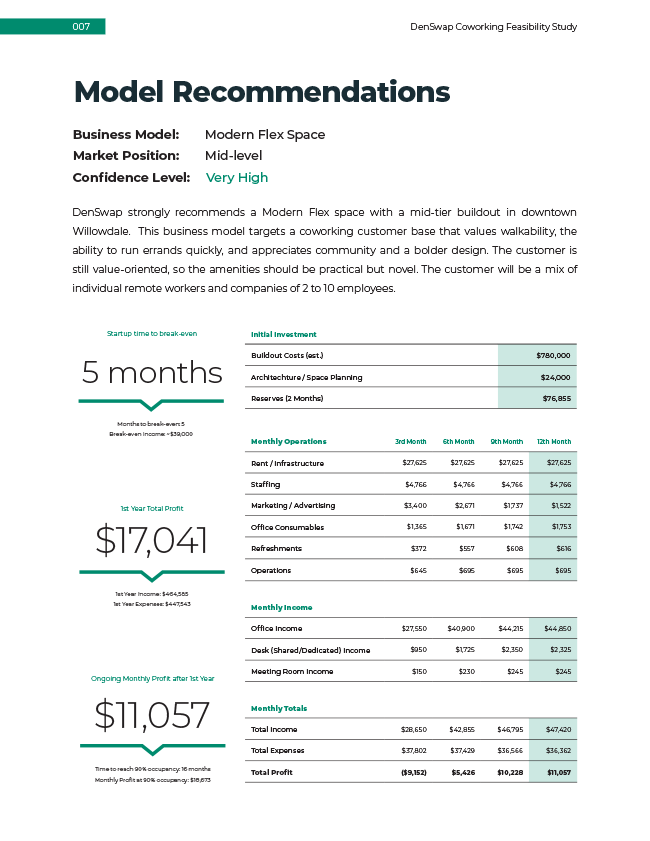

A DenSwap feasibility study answers that question directly. It maps local coworking and flex demand against your asset's physical reality, competitive set, and financial targets. Revenue projections, space allocation, pricing strategy, buildout budget, and a two-year proforma built around your specific building. Not a market overview. A decision tool.

You can download a sample feasibility study to see exactly what the analysis delivers.

Owners who test alignment before committing keep their options open and their capital intact. The ones who skip that step often spend money reinforcing the very misalignment that started the decline - and by the time they figure that out, the window for a clean repositioning has already closed.