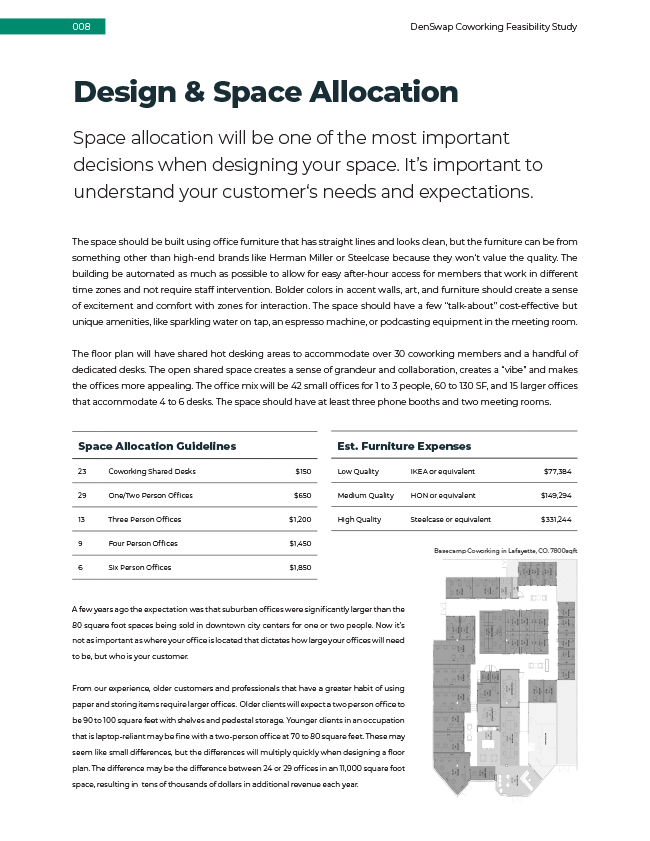

Quarter after quarter, the traditional tenant base thins out. A broker walks a partially vacant mid-size office building and suggests flex conversion. The owner pulls up a spreadsheet, compares occupancy rates, adjusts for shorter lease terms, and concludes the revenue profile looks competitive. What never gets priced is the staffing model, the amenity threshold, the churn management cost, and the technology layer that flex tenants expect from day one. The moment those costs land, the economics no longer resemble the original comparison.

This scenario plays out with increasing frequency as office vacancy rates remain elevated nationally and owners search for strategies to reactivate underperforming square footage.[1] A revenue-line comparison between flex and traditional leasing appears straightforward. The problem is that it's structurally incomplete, because the two paths don't share a cost architecture. Owners who frame flex conversion as a leasing decision will consistently underestimate what it costs to operate, because flex is a business model shift, not a lease structure swap, and the economics only justify the investment when the operational layer was fully priced before the buildout commitment was made.

The Comparison That Keeps Getting Run Wrong

The standard flex evaluation starts with two numbers: traditional occupancy at market rent versus projected flex occupancy at a per-desk or per-office rate. On paper, flex often wins. Higher per-square-foot revenue at stabilization, lower single-tenant concentration risk, and a demand pool that includes companies too small or too short-term for conventional leases.

That comparison is accurate as far as it goes. The issue is where it stops.

The revenue side of flex is a gross number. The cost side of traditional leasing is a net number. Comparing them directly is like comparing a hotel's room rate to an apartment's monthly rent and concluding the hotel is more profitable without accounting for housekeeping, the front desk, the booking system, and the breakfast bar.

When the evaluation stays at the revenue layer, flex looks like a superior lease structure. Price the operational architecture required to deliver that revenue, and the margin picture changes substantially. The question that matters is not which model generates more gross revenue per square foot. Which model generates more net operating income after the full cost of delivery?

The revenue side of flex is a gross number. The cost side of traditional leasing is a net number. That gap is where buildout capital goes to disappear.

What Each Path Actually Delivers and Costs

Traditional leasing concentrates risk into a small number of credit assumptions. Underwrite the tenant, sign a multi-year term, collect rent with relatively low operational involvement. Property management exists, but the per-tenant service burden is minimal. The economics are predictable on a per-square-foot basis, and the cost structure scales with the building, not with tenant experience expectations.

Flex distributes risk across many tenants. That diversification is real and valuable, particularly in markets where single-tenant demand has weakened.[2] But distributing risk also converts the owner's role entirely. No longer a landlord collecting rent from a creditworthy tenant on a long-term basis. Now a service operator managing short-duration relationships with high expectations for environment, technology, and responsiveness.

Supporting that role costs money across several specific line items: community management or on-site staffing, booking and access technology, internet and AV infrastructure at a commercial grade, shared amenity provisioning, and ongoing marketing and member acquisition spend. None of these exist in a traditional lease pro forma. All of them are non-negotiable in a flex operation that intends to compete against established operators.

The global coworking market is projected to grow significantly through the next decade, which confirms the demand trajectory.[3] Demand trajectory and asset-level profitability are different questions, though. The market can grow while individual conversions lose money, and the conversions that lose money are almost always the ones where the operational cost layer was underwritten after the buildout check cleared, not before.

Where the Economics Break Down

Three specific points of comparison failure surface repeatedly in flex conversions that underperform.

First, utilization assumptions. Flex pro formas frequently model stabilized occupancy without adequately pricing churn. Traditional leases have renewal cycles measured in years. Flex memberships turn over in months. A 90% occupancy rate that requires replacing 30% of the member base annually is not the same economic outcome as a 90% occupancy rate built on five-year leases. Acquiring, onboarding, and retaining flex tenants is a recurring operating expense that compresses margin in ways that traditional vacancy reserves do not capture.

Second, amenity and technology costs. The threshold for what flex tenants consider baseline has risen steadily. High-speed internet, printing, conferencing technology, and shared kitchen amenities are table stakes. Many operators report that members evaluate spaces on the quality of the technology and community experience before they evaluate price. These costs are real, ongoing, and scale with member expectations rather than square footage.

Third, management overhead. A traditional office building with five tenants on long-term leases needs a property manager and a lease administrator. A flex space with sixty members on monthly agreements needs community management, sales and marketing capability, event programming, higher-frequency maintenance, and a technology stack to manage bookings, access, and billing. This is a hospitality operation. Hospitality operations carry hospitality cost structures.

Regional banks and institutional lenders are already applying tighter scrutiny to office assets with unclear repositioning plans.[4] The capital environment does not reward incomplete underwriting, and a flex conversion approved on revenue projections without a fully loaded operating budget is precisely the kind of repositioning that stalls mid-execution.

Flex distributes tenant risk. It also distributes cost across a dozen line items that traditional underwriting has no template for.

The Right Path Depends on the Asset, Not the Trend

Asking which model is "better" in the abstract produces an answer useless for any specific asset. The productive version of the question is: can this building, in this market, at this cost basis, support the operational model that flex requires and still deliver acceptable returns?

Answering that requires stress-testing demand depth, competitive positioning against existing flex operators, realistic churn and acquisition cost modeling, and a fully loaded operating budget that includes every line item the flex model demands. If the answer is yes, flex conversion can be a strong capital decision. If no, the owner is better served pursuing traditional leasing strategies, partial repositioning, or alternative uses that match the asset's actual cost structure.

Committing capital to a buildout before the comparison is complete carries a specific kind of exposure the other risks don't. A flex conversion that discovers its operating costs six months after opening has already spent the buildout budget and cannot easily revert. A traditional leasing strategy that ignores weakening demand has its own risks.[5] Both paths carry exposure. Only one of them requires the owner to fund an entirely new operational infrastructure before revenue begins.

DenSwap's feasibility reports stress-test the economics, the asset fit, and the competitive landscape before the buildout commitment is made. The cost of that evaluation is small relative to the cost of discovering the operational gap after capital is deployed. Validate the demand depth and the cost structure first. The buildout will still be there when the numbers actually support it.