The Question Nobody Asks Before Breaking Ground

The broker's pitch usually arrives before the hard question does. By the time an owner in a secondary market has sat through a coworking repositioning presentation, a buildout is already taking shape in the back of their mind. An operator gets shortlisted. A capital plan gets drafted. The one question that should lead the whole process ends up somewhere behind the momentum: can this submarket generate the recurring membership demand required to reach breakeven? That question gets answered eventually. By the utilization numbers. After the capital is spent.

This sequence is playing out across secondary and tertiary markets right now, and the core error is the same every time. Owners are treating a demand-density business as a vacancy solution.

Office vacancy rates climbed above 13% nationally through 2024, with secondary markets hit particularly hard.[1] Coworking and flex space are growing categories. The conclusion feels inevitable: convert the empty floors, capture the trend. But that reasoning skips the only variable that determines whether the conversion produces returns or accelerates losses. Local demand depth.

Coworking does not absorb vacancy. It monetizes density. The economics of those two things are completely different, and collapsing them is where capital gets destroyed in this cycle.

Where the Economics Actually Break

The margin structure of coworking is unforgiving. Buildout capital expenditure is fixed. Operating costs, from staffing to technology to common area maintenance, are sticky. Revenue is entirely contingent on recurring occupancy that the local market may or may not produce.[2]

Most coworking operations need sustained utilization above 70% to cover operating expenses and begin servicing the buildout investment. That threshold is not a planning target. It is a survival line. And reaching it requires a specific density of local demand: enough businesses, freelancers, and remote workers within a realistic drive time who are actively seeking flexible workspace and willing to pay recurring membership fees.

The failure point in most coworking conversions is not buildout execution. It is the demand assumption that preceded it.

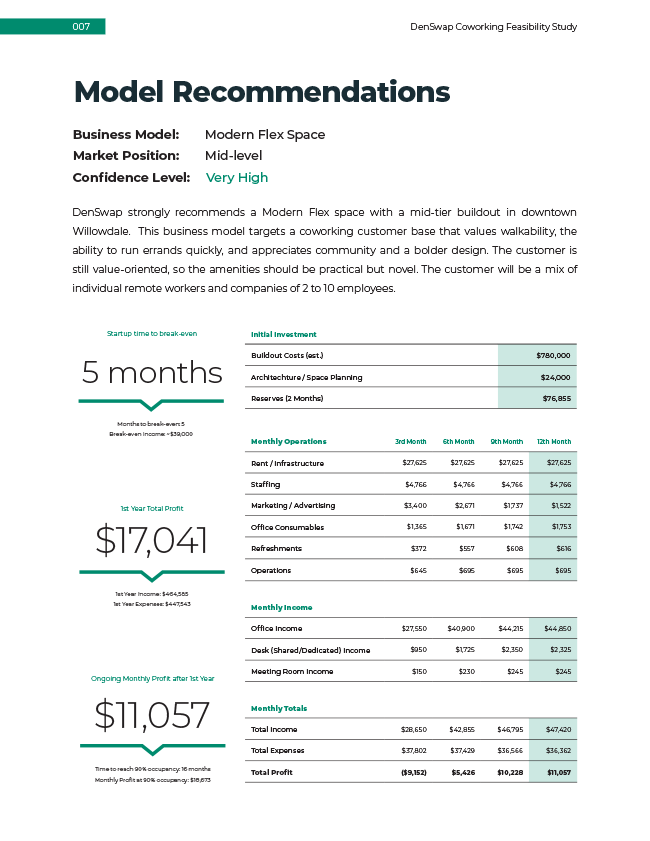

When an owner commits $150 to $250 per square foot in buildout capital based on an untested demand thesis, they are making a leveraged bet on a utilization rate they have not modeled against actual local conditions. The buildout cost is visible. The demand risk is not. That asymmetry is where capital gets destroyed.

Wheaton's analysis of coworking economics reinforces this point. The model's viability hinges on whether a given location can sustain the occupancy premium that justifies the operational overhead layered on top of a traditional lease structure.[3] Where that demand exists, the economics hold. Where it doesn't, no amount of operational competence or buildout quality closes a utilization gap baked into the submarket itself.

The Three-Part Stress Test Before Capital Is Committed

Owners considering coworking need a decision filter, not a feasibility narrative. Three conditions must hold simultaneously. If any one fails, the conversion should not proceed.

1. Local demand depth. Is there a measurable, sufficient population of potential coworking users within the asset's competitive radius? This means employed professionals in flex-compatible roles, small businesses that have outgrown home offices but cannot commit to traditional leases, and remote workers from larger firms. The question is quantitative, not qualitative. How many potential recurring members exist, and what share can you realistically capture?

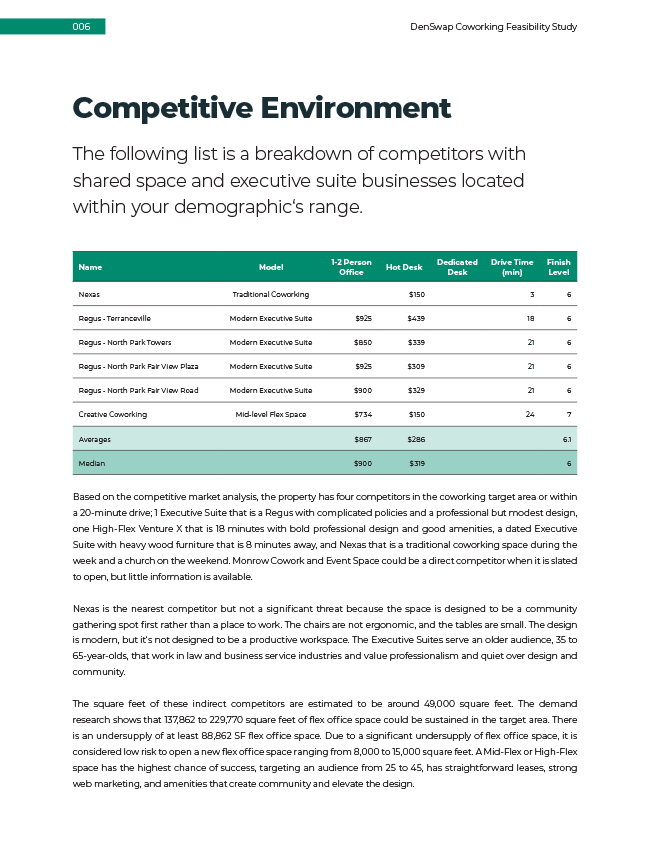

2. Competitive saturation. What is the existing supply of flexible workspace within that same radius, and how full is it? A submarket with three underperforming coworking spaces does not signal unmet demand. It signals oversupply. A submarket with one full operator and a waitlist, on the other hand, tells you something actionable. The risk-adjusted play is to compare the available demand pool against existing and planned supply, not to assume your entry creates new demand.

3. Asset-to-use-case fit. Does the physical asset match what coworking tenants actually need? Floor plates, ceiling heights, natural light, parking ratios, transit access, ground-floor visibility, and adjacency to retail and food service all factor into whether a location can attract and retain members.[4] A Class B suburban office with poor highway access and no walkable amenities faces a structural disadvantage that no interior design budget overcomes.

Each of these is a binary gate. Pass all three, and the conversion merits financial modeling. Fail one, and the capital is better deployed elsewhere.

Coworking conversions fail quietly. Weak utilization does not announce itself. It compounds over 18 months until the exit options are worse than the vacancy problem that started the whole process.

The Compounding Cost of Skipping Demand Validation

The industry's growth trajectory is real. The global flexible workspace market is projected to expand significantly through the next decade, driven by structural shifts in how businesses consume office space.[5] None of that macro momentum guarantees that a specific submarket, a specific building, and a specific capital plan will produce a return.

The downside path is predictable once you see it. Buildout cost locks the owner into a use case that is harder to reverse than traditional office. Coworking-specific improvements, from open floor plans to phone booths to shared kitchen infrastructure, do not reconvert cheaply. When utilization underperforms, the owner faces a choice between subsidizing operations to maintain the space or writing off the buildout to re-lease conventionally. Both paths are more expensive than the vacancy problem the conversion was supposed to solve.

The Avison Young research on landlord-operator risk sharing highlights the trend toward owners taking on more direct exposure to coworking performance.[6] That exposure makes demand validation existential, not optional. When the owner absorbs utilization risk, the demand thesis is the underwriting. Underwriting without data is speculation.

The cheapest capital protection available before a coworking buildout is not a better operator or a more efficient floor plan. Knowing whether the demand exists at all is. That question is measurable. The demographics, the competitive landscape, the total addressable market for flexible workspace within your asset's radius: all of this can be quantified before a single dollar of buildout capital is committed. A DenSwap demand report delivers that validation in 24 hours for $500, covering local demographics, supportable coworking square footage, and recommended business models. You can download a sample here to see exactly what the analysis covers. If the demand numbers are solid, then the cost can be credited towards a more complex DenSwap feasibility report, which additionally covers the deeper competitive saturation, asset-to-use-case buildout, and financial projections.

Five hundred dollars to test the demand thesis before committing six figures in buildout. That is not analysis. That is capital discipline.